Publications

``Private versus Social Responses to a Pandemic, Journal of Economic Dynamics and Control, December 2025, 181, pages 105202.

Abstract: What are the socially optimal restrictions on private activity during a pandemic? How do these differ from private decisions? We address these questions by modeling the interactions between epidemiology and the macroeconomy. Unlike the private planner, the social planner accounts for two externalities: the increase in the cost of severe illness associated with more infected individuals, reflecting the capacity constraints of the health care system; and the socioeconomic transmission of the virus from asymptomatic to susceptible individuals. Owing to these externalities, the social planner imposes stricter constraints on socioeconomic activities. Applied to the COVID-19 pandemic, socially optimal restrictions reduce the welfare costs by roughly one percent of GDP.

``U.S. Fiscal Policy During and After the Coronavirus'', Canadian Journal of Economics, February 2022, 55(S1), pp. 358-378.

Abstract: COVID-related government outlays will increase the level of government debt. A macroeconomic model, calibrated to the U.S., quantitatively assesses potential responses to this higher debt. In terms of economic welfare, reducing debt through capital incomes tax hikes is the least desirable option considered: the associated tax base is small, and anticipating such a tax increase reduces capital accumulation. There is little to choose between fiscal austerity through government spending cuts versus raising labor income tax rates. Accommodating higher government debt is welfare-improving, but still requires substantial fiscal auserity owing to higher debt servicing costs.

``COVID-19 Pandemic and Economic Scenarios for Ontario'' (with Midel Casares and Hashmat Khan), Canadian Journal of Economics, February 2022, 55(S1), pp. 503-539.

Abstract: To study the efficacy of the public policy response to the COVID-19 pandemic, we develop a model of the rich interactions between epidemiology and socioeconomic choices. Preferences feature a ``fear of death'' that lead individuals to reduce their social activity and work time in the face of the pandemic. The aggregate effect of these reductions is to slow the spread of the coronavirus. We calibrate the model, including public policies, to developments in Ontario in spring 2020. The model fits the epidemiological data quite well, including the second wave starting in late 2020. We find that socioeconomic interventions work well in the short term, resulting in a rapid drop off in new cases. The long run, however, is governed chiefly by health developments. Welfare cost calculations point to synergies between the health and socioeconomic measures.

``Debt Hangover in the Aftermath of the Great Recession'' (with Stephane Auray and Aurelien Eyquem), Journal of Economic Dynamics & Control, August 2019, 105, pp. 107-133.

Abstract: Following the Great Recession, U.S. government debt levels exceeded 100% of output. We develop a macroeconomic model to evaluate the role of various shocks during and after the Great Recession; labor market shocks have the greatest impact on macroeconomic activity. We then evaluate the consequences of using alternative fiscal policy instruments to implement a fiscal austerity program to return the debt-output ratio to its pre-Great Recession level. Our welfare analysis reveals that there is not much difference between applying fiscal austerity through government spending, the labor income tax, or the consumption tax; using the capital income tax is welfare-reducing.

``Ramsey-optimal Tax Reforms and Real Exchange Rate Dynamics'' (with Stephane Auray and Aurelien Eyquem), Journal of International Economics, November 2018, 115, pp. 159-169.

Abstract: We solve the Ramsey-optimal tax plan for a small open economy with an endogenously-determined real exchange rate. The open economy constrains the government's setting of the capital income tax rate since physical capital cannot be dominated in rate of return by foreign assets. However, the endogenous real exchange rate loosens this constraint relative to a one good open economy model in which the real exchange rate is necessarily fixed. We find that, the dynamics of the two good small open economy model more closely resemble those of a closed economy model than a one good small open economy model.

Code: Fortran code for Ramsey-optimal tax policies

``Market Work, Housework and Childcare: A Time Use Approach'' (with Emanuela Cardia), Review of Economic Dynamics, July 2018, 29(1), pp. 1-14.

Amstract: Raising children takes considerable time, particularly for women. Yet, the role of childcare time has received scant attention in the macroeconomics literature. We develop a life-cycle model in which the time dimension of childcare plays a central role. An important contribution of the paper is estimation of the parameters of a childcare production function using data on primary and secondary childcare time as reported in the American Time Use Survey (2003--2015). The model does a better job matching the observed life-cycle patterns of womens' time use than a model without childcare. Our counterfactual experiments show that the increase in the relative wage of women since the 1960s is an important factor in the increase in womens' work time; changes in fertility associated with the baby boom play a smaller role, and changes in the price of durables are found to have a negligible effect. We consider the effects of cheaper daycare. Not surprisingly, this experiment leads to greater use of daycare and more time allocated to market work. A knock-on effect of cheaper daycare is a substantial decline in primary childcare time.

Code:

- R code to compute the distribution used in the Fortran code,

- R code to compute Table 1,

- R code to estimate the childare production function parameters,

- Fortran code to compute the model.

``A Tale of Tax Policies in Open Economies'' (with Stephane Auray and Aurelien Equyem), International Economic Review, November 2016, 57(4), pp. 1299-1333.

Abstract: Tax-based deficit reduction experiments for the U.S. and EMU-12 are conducted using an open economy model. In welfare terms, raising the consumption tax is the least costly, followed by the labor income tax, then the capital income tax. Use of an open economy model means that the incidence of the consumption tax is borne in part by foreign producers. Among revenue-neutral tax experiments, partially replacing the capital income tax is welfare-enhancing, although there are short term losses. Replacing labor income tax revenue with a consumption tax improves international competitiveness and is welfare-improving.

``Worker Search Effort as an Amplification Mechanism'' (with Damba Lkhagvasuren) Journal of Monetary Economics, October 2015

Abstract: It is well known that the Diamond-Mortensen-Pissarides model exhibits a strong trade-off between cyclical unemployment fluctuations and the size of rents to employment. Introducing endogenous job search effort reduces the strength of the trade-off while bringing the model closer to the data. Ignoring worker search effort leads to a large upward bias in the elasticity of matches with respect to vacancies. Merging the American Time Use Survey and the Current Population Survey, new evidence in support of procyclical search effort is presented. Average search effort of the unemployed is subject to cyclical composition biases.

``Measuring the Welfare Costs of Inflation in a Lifecycle Model'', Journal of Economic Dynamics and Control, August 2015, pages 132-144.

Abstract: In a neoclassical growth model with life-cycle households in which money is held to satisfy a cash-in-advance constraint, the optimal steady state inflation rate is absurdly high: in excess of 20%. Lump-sum, age-independent money injections twist and flatten the lifetime profile of utility, making this profile look more like the one that would be chosen by a planner. The cost of monetary finance of lump-sum payments is the distortion introduced to the labor-leisure choice.

``Calibration and Simulation of DSGE Models'' (with Damba Lkhagvassuren), in Handbook of Research Methods and Applications in Empirical Methods in Macroeconomics, Nigar Nasimzade and Michael Thornton, eds. (Edward Elgar), pp. 575-592.

Data (updated May 2022): Python file

Amazon.com link. An early draft.

``Nominal Rigidities, Monetary Policy and Pigou Cycles'' (with Stephane Auray and Shen Guo) Economic Journal, 123 (568), May 2013, pages 455-473.

Abstract: Capturing the boom phase of Pigou cycles and resolving the comovement problem requires positive sectoral comovement. This paper addresses these observations using a two sector New Keynesian model. Price rigidities dampen movements in the relative price of durables following a monetary policy shock. Durables and nondurables are estimated to be complements in utility, allowing for a resolution of the comovement problem for modest degrees of price rigidity. Nominal rigidities also make firms forward-looking in their pricing behaviour which leads to relative price dynamics that generate positive sectoral comovement in the boom phase of a Pigou cycle.

``Second-order approximation of dynamic models without the use of tensors'' (with Paul Klein) Journal of Economic Dynamics and Control 35 (4), April 2011, pages 604-615.

Abstract: Several approaches to finding the second-order approximation to a dynamic model have been proposed recently. This paper differs from the existing literature in that it makes use of the Magnus and Neudecker (1999) definition of the Hessian matrix. The key result is a linear system of equations that characterizes the second-order coefficients. No use is made of multi-dimensional arrays or tensors, a practical implication of which is that it is much easier to transcribe the mathematical representation of the solution into usable computer code.

Matlab code is available from http://paulklein.se/codes.php; Fortran 90 code for the basic routines for first- and second-order approximations.

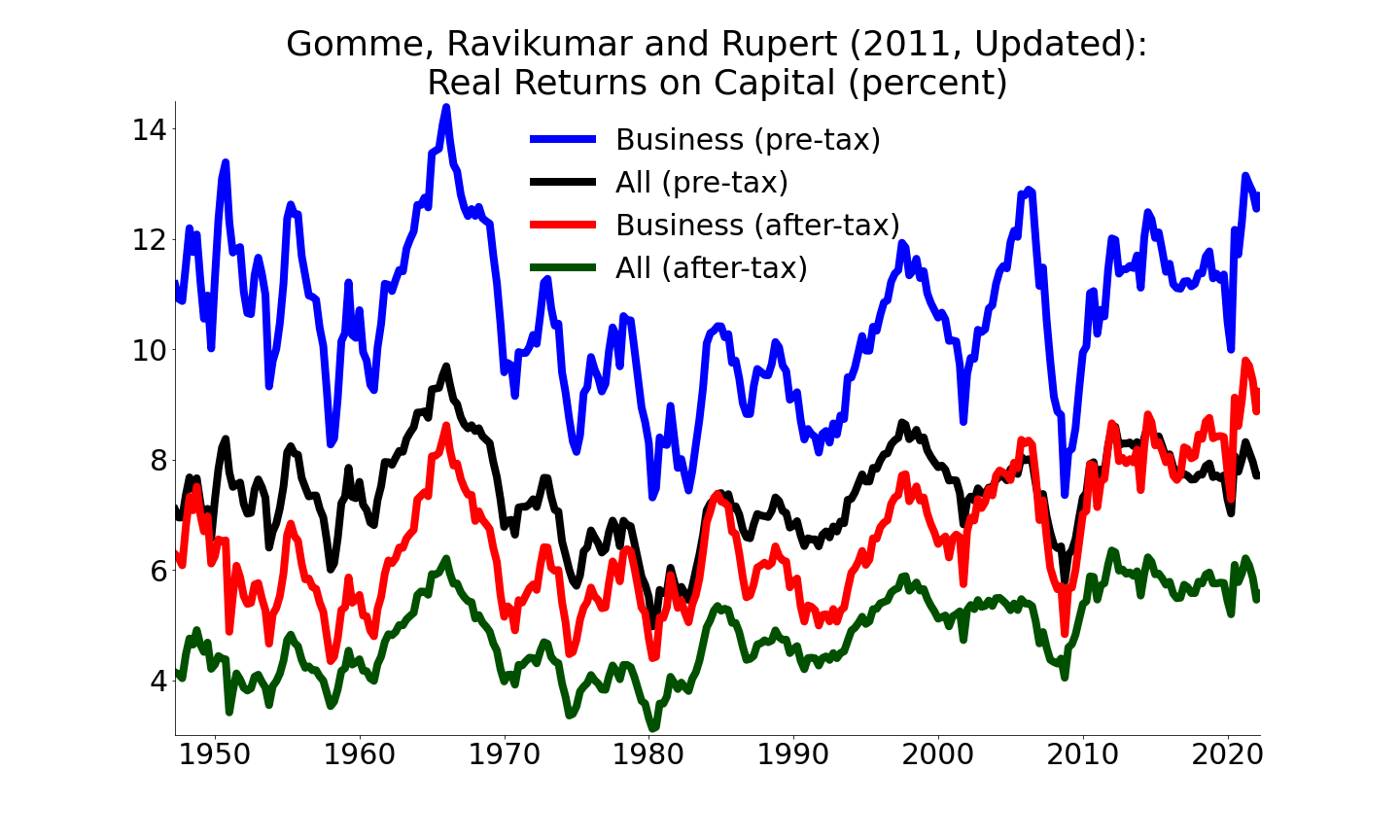

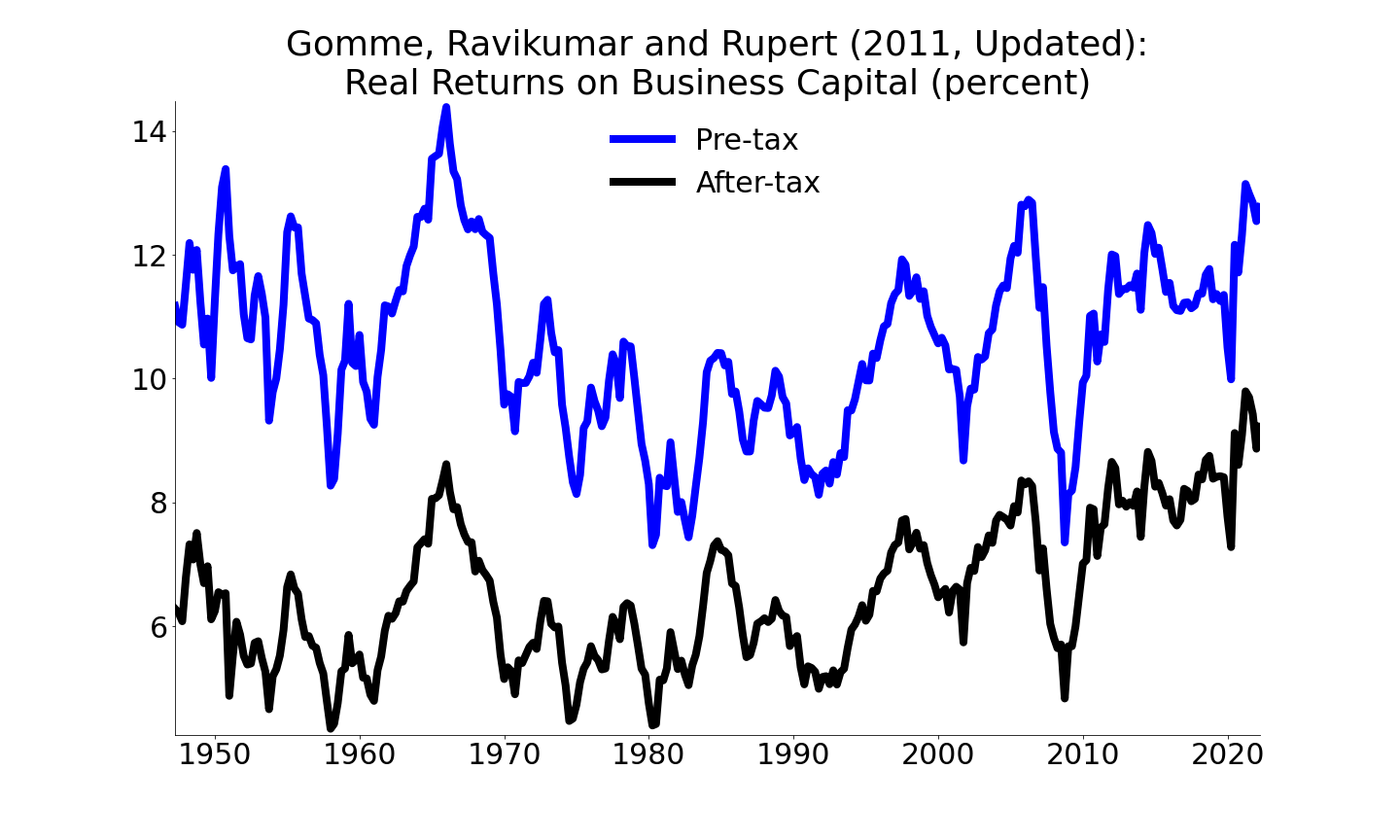

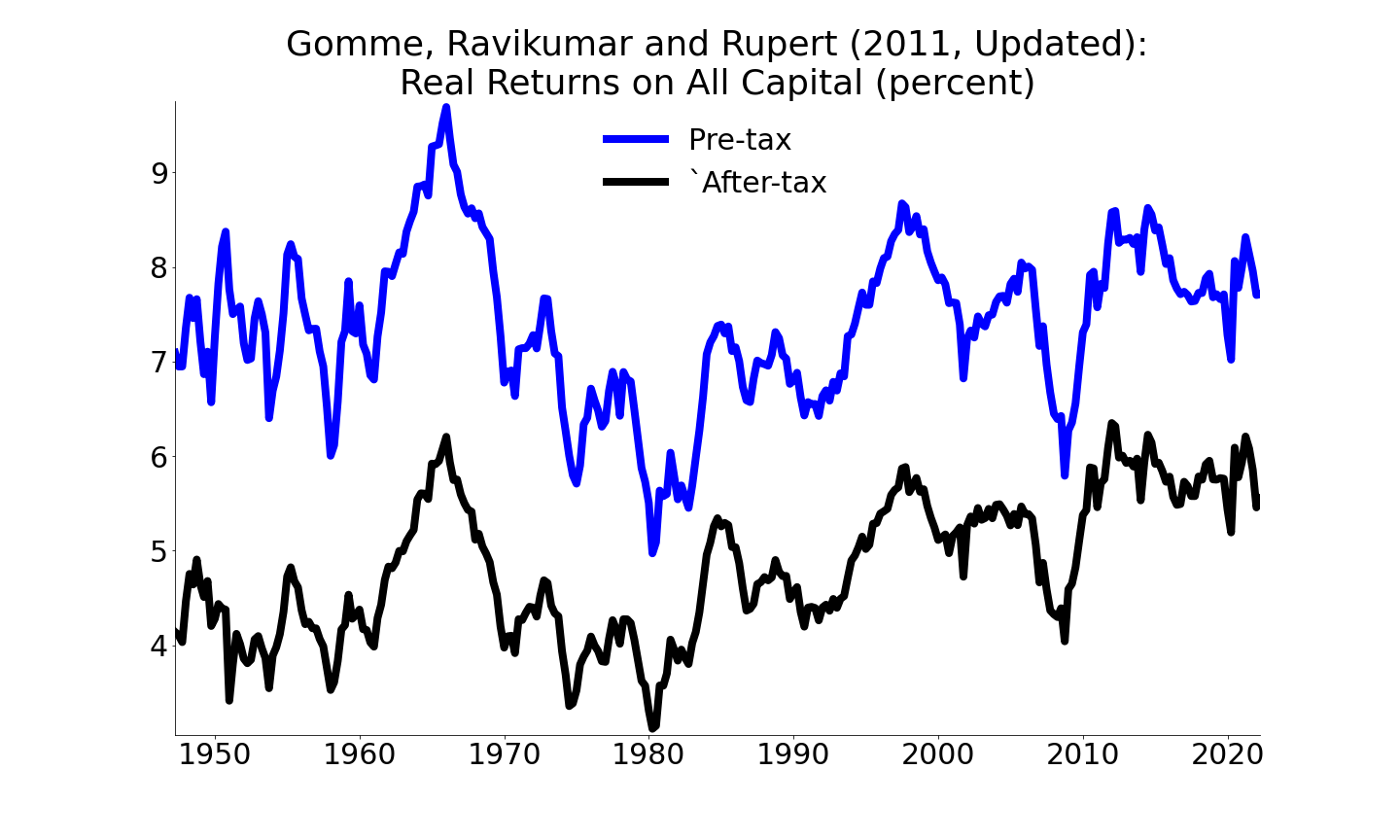

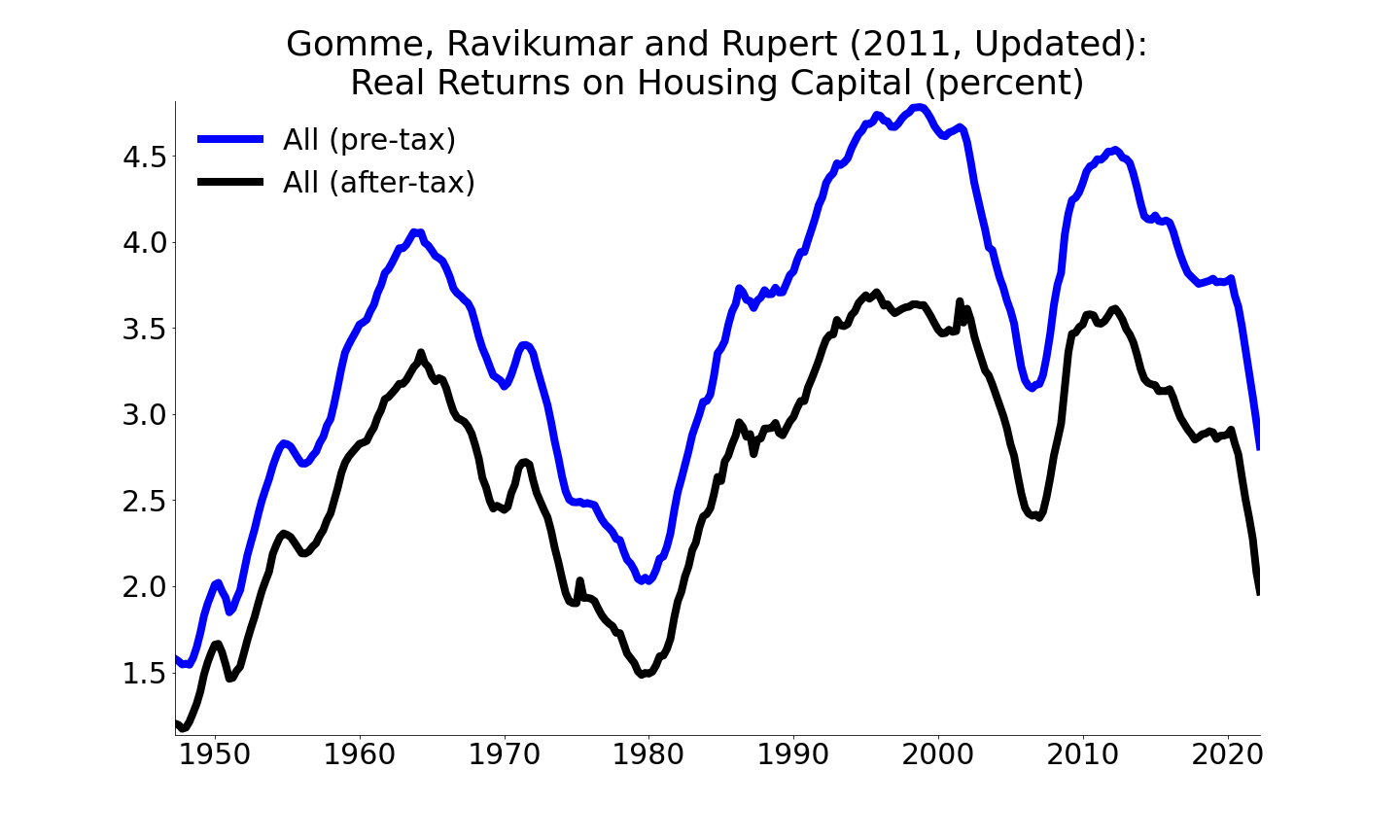

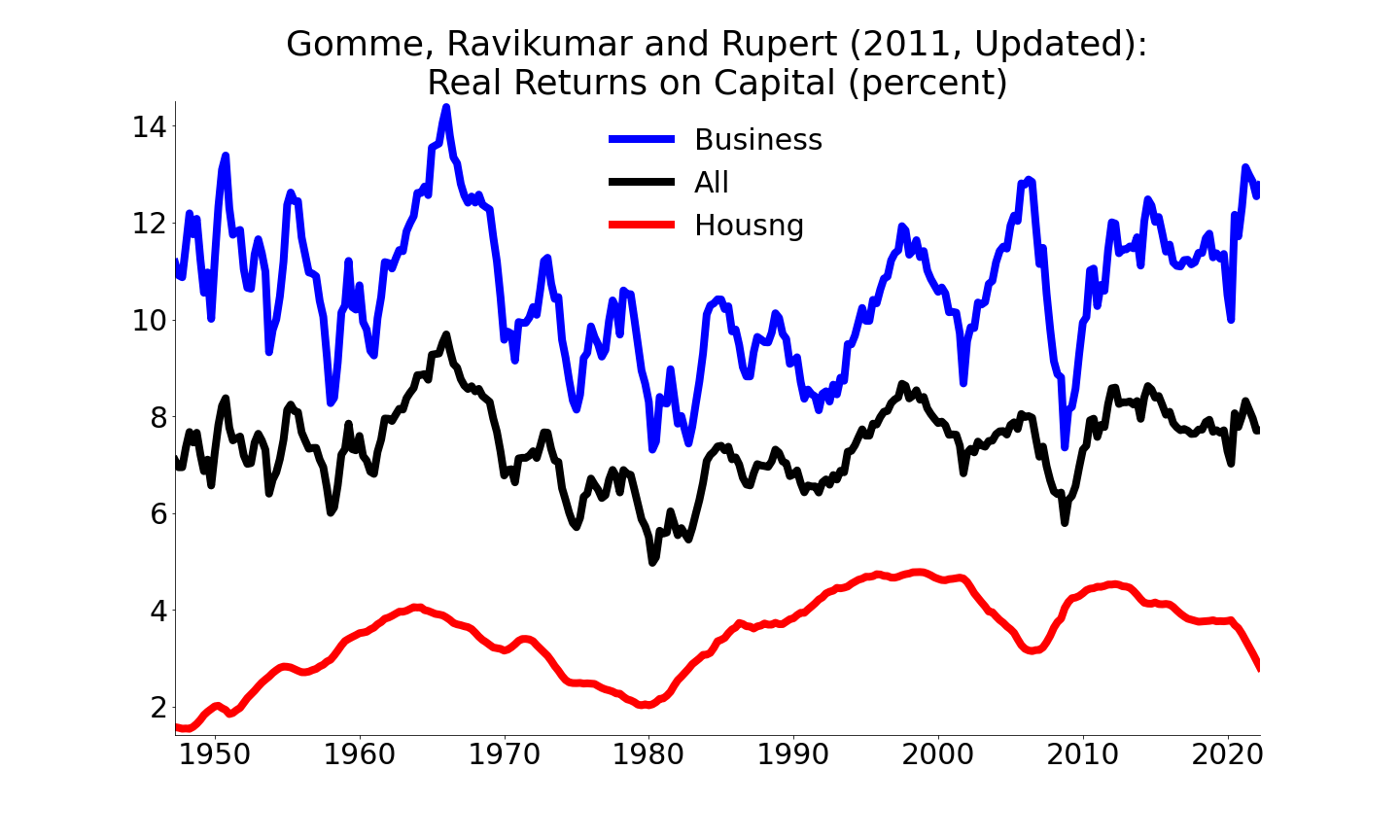

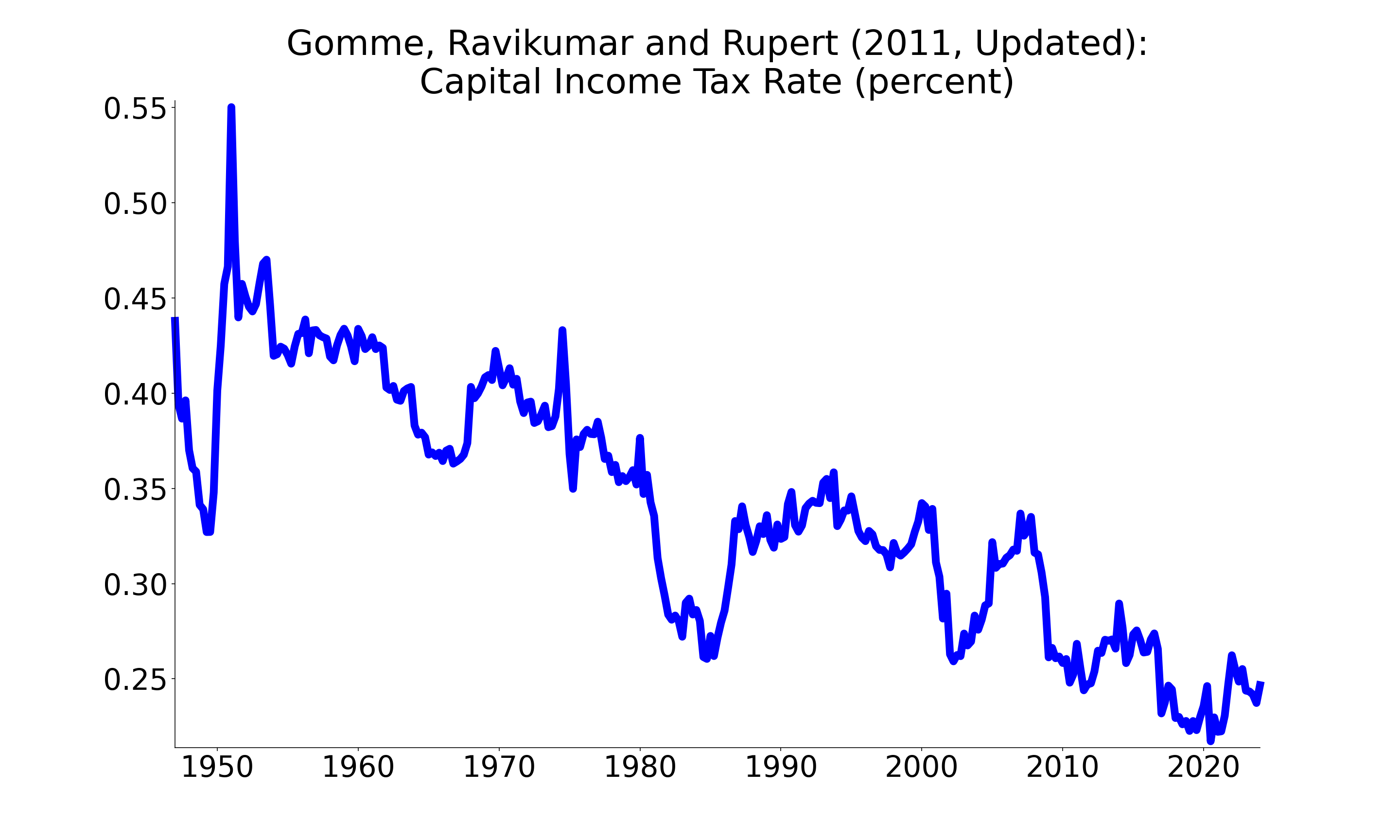

``The Return to Aggregate Capital and the Business Cycle'' (with B. Ravikumar and Peter Rupert) Review of Economic Dynamics 14 (2), April 2011, pages 262-278.

Data (updated July 2022): Python code.

Abstract: A widely cited failing of real business cycle models is their inability to account for the cyclical patterns of financial variables. Perhaps less well known is the fact that the return to capital and equity are identical in the neoclassical growth model. This paper constructs a measure of the return to business capital for the U.S. The S&P 500 return is roughly six times more volatile than the return to business capital. Owing to the equivalence between the returns to capital and equity in the neoclassical growth model, papers in the real business cycle literature that successfully account for the time series variation in the S&P 500 return must fail to account for the time series properties of the return to capital. A fairly basic real business cycle model captures most of the observed variability in the return to capital. What is needed is a theory of the stock market that breaks the equivalence between the returns to equity and capital.

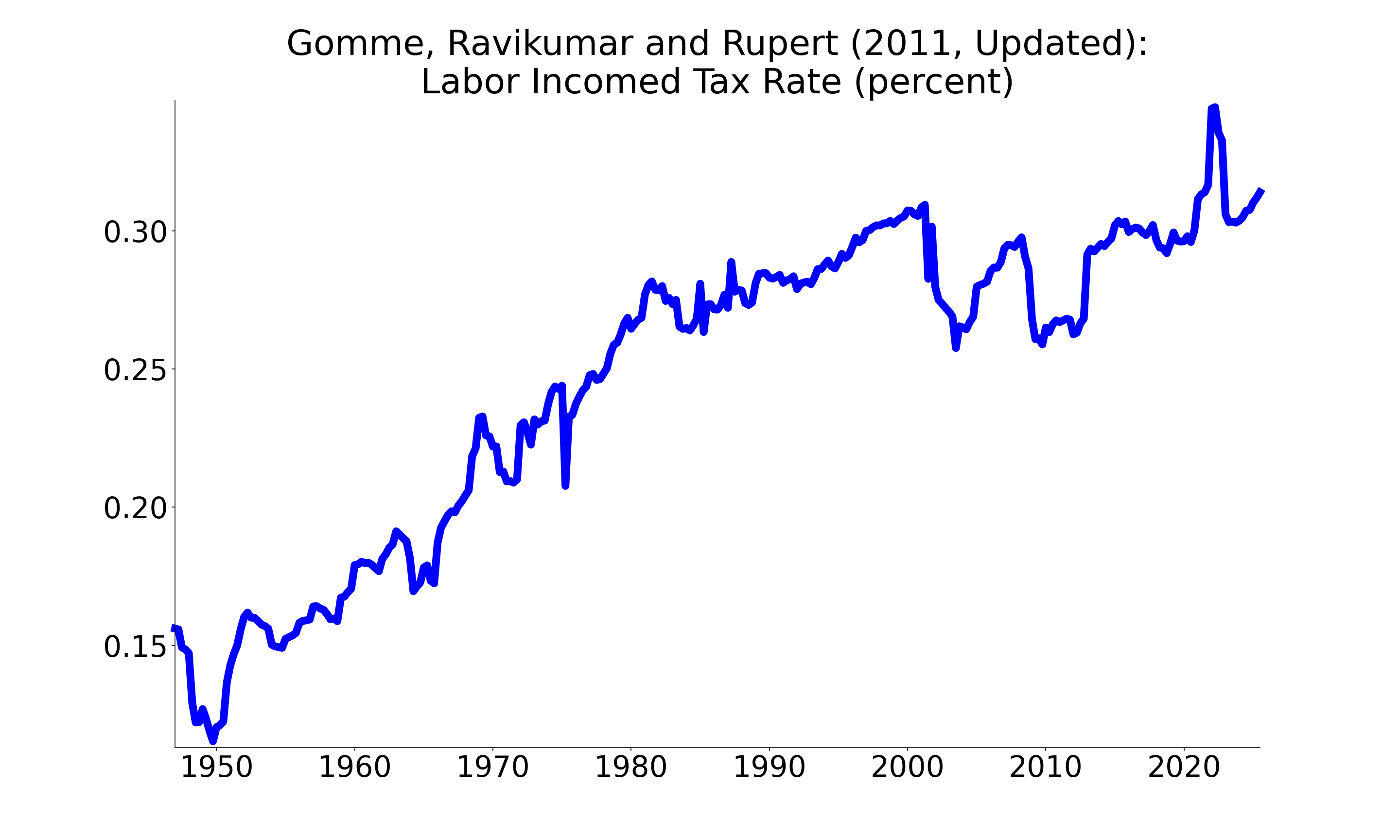

``Theory, Measurement and Calibration of Macroeconomic Models'' (with Peter Rupert) Journal of Monetary Economics 54 (2), March 2007, pages 460-497.

Data (updated May 2022): Python code

Abstract: Calibration has become a standard tool of macroeconomics. This paper extends and refines the calibration methodology along several important dimensions. First, accounting for home production is important both in measuring calibration targets and in organizing the data in a model-consistent fashion. For this reason, thinking about home production is important even if the model under consideration does not include home production. Second, investment-specific technological change is included because of its strong balanced growth parameter restrictions. Third, the measurement strategy is laid out as transparently as possible so that others can easily replicate the underlying calculations.

``The Business Cycle and the Life Cycle'' (with Richard Rogerson and Peter Rupert and Randall Wright), NBER Macro Annual 2004, pages 415-461.

Abstract: This paper explores the variation in hours of work over the life-cycle through the lens of a model incorporating home production. While the model successfully accounts for hours variation of individuals late in their life-cycle, it fails to capture the high variation in hours of work early in the life-cycle.

``Monetary Policy Regimes and Beliefs'' International Economic Review (with David Andolfatto) 44 (1), February 2003, pages 1-30.

Abstract: This paper investigates the role of beliefs over monetary policy in propagating the effects of monetary policy shocks within the context of a dynamic, stochastic general equilibrium model. In our model, monetary policy periodically switches between low and high money growth regimes. When individuals are unable to observe the regime directly, they form inferences over regime-type based on historical money growth rates. For an empirically plausible money growth process, beliefs evolve slowly in the wake of a regime change. As a result, our model is able to capture some of the observed persistence of real and nominal variables following such a regime change.

``Home Production Meets Time-to-build'' Journal of Political Economy (with Finn Kydland and Peter Rupert) 109 (5), October 2001, pages 1115-1131.

Abstract: An innovation in this paper is to introduce a time-to-build technology for the production of market capital into a model with home production. Our main finding is that the two anomalies that have plagued all household production models---the positive correlation between business and household investment, and household investment leading business investment over the business cycle---are resolved when time-to-build is added.

``Shirking, Unemployment and Aggregate Fluctuations'' International Economic Review 40 (1), February 1999, pages 3-21.

Abstract: Empirically, real wages exhibit relatively little cyclical variation and a weak cyclical pattern. Early real business cycle models predict, to the contrary, large, procyclical real wage movements. Incorporating efficiency wages into a real business cycle environment would seem promising since one prediction from the efficiency wage literature is real wage rigidity. This paper evaluates a common microfoundation for efficiency wages, the shirking model, with respect to its predictions for real wages within a real business cycle-style model. Simulations of the model reveal that it can generate dampened, but still strongly procyclical real wage behavior.

``Applying Evolutionary Programming to Selected Set Partitioning Problems'' International Journal for Fuzzy Sets and Systems (with Paul Harrald) 95 (1), April 1, 1998, pp. 67-76.

Abstract: Evolutionary programming is applied to several instances of the set partitioning problem. Comparison is made between the distribution of best-evolved solutions arising from implementations of the EP with the empirical distribution of a randomly selected trial solution.

``U.S. Labour Market Policy and the Canada--U.S. Unemployment Rate Gap'' Canadian Public Policy (with David Andolfatto and Paul Storer) 24 (S1), February 1998, pp. 210-232.

Abstract: In this paper, we investigate the extent to which changes in U.S. labour market policy in the 1980s may have contributed to the emergence of an unemployment rate gap between Canada and the United States. In that decade, unemployment insurance benefits became taxable, income tax rates fell substantially, and various administrative changes were made that effectively tightened unemployment insurance eligibility requirements. These policy changes are evaluated in the context of a computable equilibrium model of the labour market. Our estimates suggest that all of these reforms together can account for no more than a 0.4 percentage point decline in U.S. natural rate of unemployment; a combined effect which accounts for 20 percent of the unemployment rate gap.

``Unemployment Insurance and Labor-market Activity in Canada'' Carnegie-Rochester Conference Series on Public Policy, (with David Andolfatto), 44, June 1996, pp. 47-82.

Abstract: In 1972, the Canadian Federal government implemented a wide-ranging set of reforms to the nation's unemployment insurance system. The economic impact of these reforms are evaluated in the context of a dynamic general equilibrium model of labor-market search. A calibrated version of the model estimates that the 1972 reforms had only a modest impact on unemployment, but led to a significant increase in the rate of labor-market turnover, particularly on flows into and out of the labor force. The model also estimates that on net, the reforms likely contributed to an increase in social welfare by reducing the level of idiosyncratic income risk.

``On the Cyclical Allocation of Risk,'' Journal of Economic Dynamics and Control (with Jeremy Greenwood), 19 (1), January 1995, pp. 91-124.

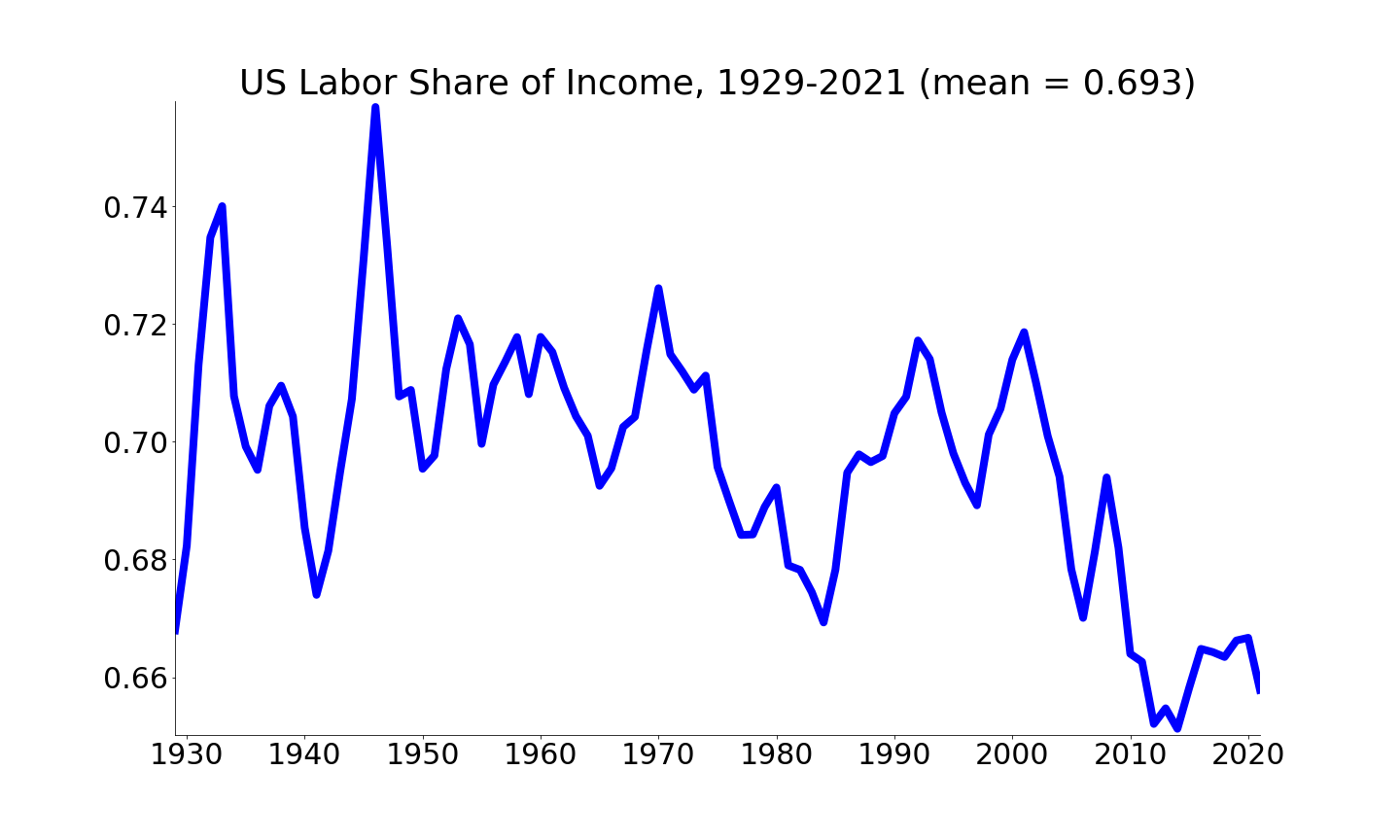

Abstract: A real business cycle model with two types of agents, workers and entrepreneurs, is simulated to see if it can account for some stylized facts characterizing postwar U.S. business cycle fluctuations, such as the countercyclical movement of labor's share of income, and the acyclical behavior of real wages. It can. There exists an economy-wide market for contingent claims. On this market workers purchase insurance from entrepreneurs, through optimal labor contracts, against losses in income due to business cycle fluctuations. Insurance flows protecting workers against aggregate cyclical risk are calculated to be less than one percent of labor income.

``Labor Turnover and the Natural Rate of Unemployment: Efficiency Wage vs Frictional Unemployment,'' Journal of Labor Economics (with W. Bentley MacLeod and James M. Malcomson), 12 (2), April 1994, pp. 276-315.

Abstract: Wage and unemployment responses to changes in economic environment are compared for efficiency wage and frictional models. Changes in aggregate demand, persistence of job-specific shocks, cost of living, and unemployment benefits are considered. Wages and unemployment move in the same direction in the two models, except that an upward shift in aggregate labor demand can reduce the real wage in the efficiency wage, but not the frictional, model. In a numberical simulation calibrated to U.S. data, real productivity shocks in the efficiency wage model yield a ratio of unemployment to wage variability close to that of the United States.

``Money and Growth Revisited: Measuring the Costs of Inflation in an Endogenous Growth Model,'' Journal of Monetary Economics, 32 (1), August 1993, pp. 51-77.

Abstract: Conventional wisdom is that if public policy can affect the growth rate of the economy, the welfare implications of alternative policies will be large. In this paper, a stochastic, dynamic general equilibrium model with endogenous growth and money is examined. In this setting, inflation lowers growth through its effect on the return to work. However, the welfare costs of higher inflation are modest. The endogenous labor supply is important in producing this result.

Federal Reserve Bank Publications

Federal Reserve Bank of St. Louis

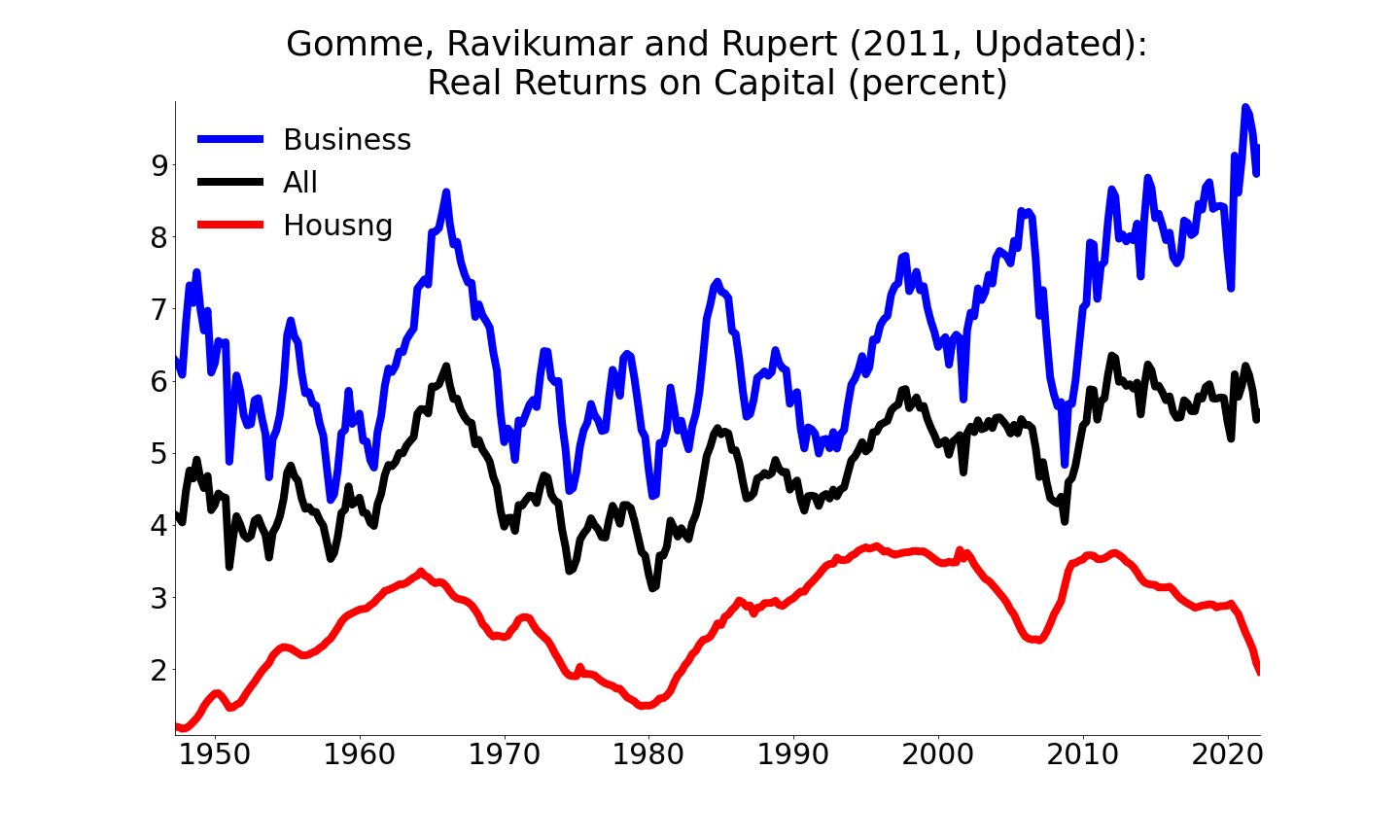

``Return to Capital in a Real Business Cycle Model'' (with B. Ravikumar and Peter Rupert), Federal Reserve Bank of St. Louis Review, 99(4), Fourth Quarter 2017, pp. 337-350.

Abstract: Can the neoclassical growth model generate fluctuations in the return to capital similar to those observed in the United States? Equating stock market returns with the return to capital, the bulk of the literature concludes that it cannot. This article makes two contributions. First is an equivalence for the neoclassical growth model between a stock market return and a return based on income and capital stock data. While the stock market return is extremely volatile, the income-based return is not. Second is the finding that the neoclassical growth model with shocks to labor productivity alone can account for the bulk of the observed volatility of the income-based return to capital (expressed relative to the volatility of income) but little of the volatility of the stock market return. Simultaneously explaining the volatility of the two measures of the return to capital within the neoclassical model will require a theory of the stock market that breaks our return-equivalence results.

``Secular Stagnation and Returns on Capital'' (with B. Ravikumar and Peter Rupert), Economic Synopses, August 18, 2015.

Data: R code., comma-separated values (CSV) data file, or text file.

Federal Reserve Bank of Cleveland

``In search of the NAIRU'' (with David Altig), Economic Commentary, May 1, 1998.

``Canada's Money Targeting Experiment'', Economic Commentary, February 1, 1998.

``What Labor Market Theory Tells Us about the `New Economy''', Economic Review 1998 Quarter 3, pages 16-24.

``Unemployment and Economic Welfare'' (with David Andolfatto), Economic Review, 1998 Quarter 3, pages 25-33.

``On the Costs of Inflation'', Economic Commentary, May 15, 2001.

``Free Trade and Tariffs-An Uneasy Mix'', Economic Commentary, September 1, 2002.

``Evaluating the Macroeconomic Effects of a Temporary Investment Tax Credit'', Policy Discussion Paper, No. 02-03, 2002.

``The Iowa Electronic Markets'', Economic Commentary, April 15, 2003.

``Per Capita Income Growth and Disparity in the United States, 1929-2003'' (with Peter Rupert), Economic Commentary, August 15, 2004.

``Why Policymakers Might Care about Stock Market Bubbles'', Economic Commentary, May 15, 2005 (reprinted in U.S. Banker, August 1 2005)

``Accounting for the Jobless Recoveries'', Economic Commentary, August 1, 2005.

``Central Bank Credibility'', Economic Commentary, August 1, 2006.